Medical bankruptcy is relatively common for Americans due to the rising cost of health care and health insurance policies. Unforeseen medical issues, job loss, and high cost medical procedures can send families into medical debt, no matter the quality of their health insurance plan.

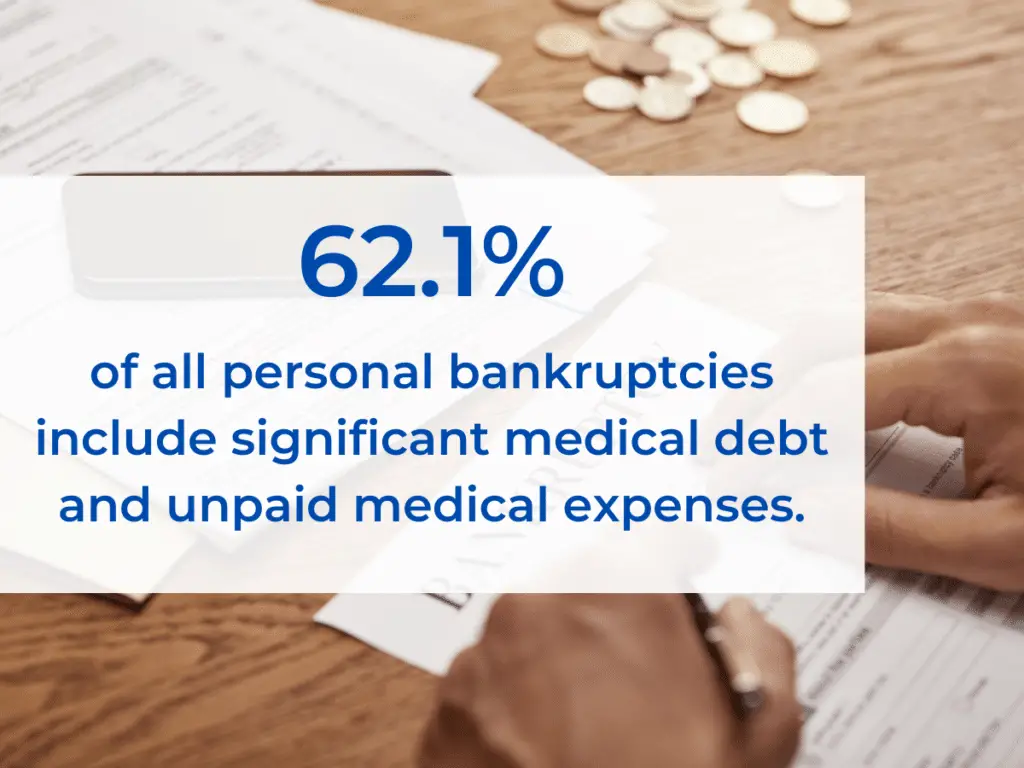

In fact, significant medical debt and unpaid medical expenses are included in roughly 62.1% of all personal bankruptcies. And this step may be the right decision for your financial situation.

So how do you get started?

If you can’t afford a bankruptcy attorney and need a fresh start, knowing the necessary steps and forms required for filing bankruptcy can help you resolve those overwhelming medical bills.

1. Collect All of Your Financial Documents

The first step you need to take in the bankruptcy process is collecting all of your financial documents to prove your income and expenses. When filing a Chapter 7 case, you must have your tax returns and proof of income from the past six months. You will also need a list of your living and medical expenses to complete the forms.

The Chapter 7 bankruptcy petition also requires you to complete a Means Test to see if you qualify to file. The test compares your income to the average household income in your state. Your average total income must be below your state’s median income to qualify for Chapter 7 bankruptcy.

2. Get Copies of Your Credit Report

The next step is to acquire copies of your credit record. In this report, you will see the list of creditors that you need to include in your bankruptcy forms, including the healthcare providers you owe. Though you might only be worried about your medical or credit card debt, you must list all priority, secured, and unsecured debts on the bankruptcy forms. You can request a copy of your credit report online for free every twelve months.

You can get a copy of your report in one of three ways:

- Get it online through AnnualCreditReport.com. This is the only website authorized by the federal government to provide online credit reports.

- Call 1-877-322-8228 to make the request with Annual Credit Report over the phone.

- Mail the request form to Annual Credit Report Request Service, PO Box 105281, Atlanta, GA 30348.

You must include all medical costs and potential medical debt at the time you file regardless if you know how much the bill will be or whether insurance will cover enough of it. You cannot claim it after your bankruptcy filing is complete, and you will be required to pay the full amount.

3. Make a List of Your Assets

You must report all the properties you own and the value of those properties in addition to debts, income, and expenses.

You may not know the value of larger and more expensive items, such as real estate and vehicles, so a tax appraisal can help you determine those values. Kelly Blue Book online and NADA are particularly useful in determining the value of your vehicles.

4. Complete the Credit Counseling Course

The bankruptcy counseling course is the first of two classes you must take when filing for bankruptcy. It must be taken from a government-approved agency, and it prepares you to fill out your documents, because it asks many of the same questions regarding your income and expenses. The course costs between $10 to $50, and you can take it online or over the phone. The course can be completed in less than two hours.

During Bankruptcy Course 1, you tell the agency your expenses and monthly income, and they review the options you may have in dealing with your debts. They can also advise you on whether an informal repayment plan might help get you back on track financially. The course is a valuable way to explore all of your options and see if bankruptcy is the right step for you.

After completing the course, you or your lawyer (if applicable) will be emailed a certificate of completion. You must file this certificate with your bankruptcy case. It is crucial that you include it; otherwise, your case may be dismissed.

5. Fill Out the Required Bankruptcy Forms

You can find the documents online at the United States Courts website. There are at least 23 separate forms where you will need to list all of your total debts, personal properties, and any real estate that you own. You will also need to record every detail of your financial life, including your marital status, all family expenses, debt payments, and total family income.

If you’re an individual debtor, these are the forms required to file a bankruptcy petition for your medical debt in America:

- Voluntary Petition for Individuals Filing for Bankruptcy

- Summary of Your Assets and Liabilities and Certain Statistical Information

- Schedule A/B: Property

- Schedule C: The Property You Claim as Exempt

- Schedule D: Creditors Who Hold Claims Secured by Property

- Schedule E/F: Creditors Who Have Unsecured Claims

- Schedule G: Executory Contracts and Unexpired Leases

- Schedule H: Your Codebtors

- Schedule I: Your Income

- Schedule J: Your Expenses

- Declaration About an Individual Debtor’s Schedules

- Your Statement of Financial Affairs for Individuals Filing Bankruptcy

- Statement of Intention for Individuals Filing Under Chapter 7

- Your Statement About Your Social Security Numbers

- Chapter 7 Statement of Current Monthly Income (only for Chapter 7 petitions)

- Chapter 7 Means Test Calculation (only if you qualify for a Chapter 7 petition)

There are optional additional forms if you plan to pay the filing fee in installments or seek to get the fee waived.

6. Pay Your Filing Fee

The American federal court charges a hefty filing fee to file a new bankruptcy petition. A new Chapter 7 petition is $335 to file, and filing a Chapter 13 bankruptcy is $310. You can either pay this fee in full on the day you file your documents, set up a plan to pay through installments, or apply for a fee waiver.

You can find the Chapter 7 filing fee waiver online and bring it to the courthouse on the day you file. Your total household income must be 150% under the federal poverty line in order to qualify for the waived fee.

7. File Your Bankruptcy Forms in Court

When you go to your local courthouse, you need to bring your bankruptcy forms and the filing fee, installment plan, or waiver. Your bank statements and other financial documents do not get submitted to the court but go to the trustee assigned to you later on.

The clerk will scan and upload your forms to the court’s online system in about 15 minutes. Once the documents are uploaded, the clerk will give you your bankruptcy case number, your bankruptcy trustee’s name, and the details regarding your meeting with the trustee of your case, otherwise known as the 341 meeting.

Once you have filed, you won’t have to worry about collectors or notices reminding you to pay your medical bills. However, your bankruptcy journey is not over yet.

8. Mail Your Financial Documents to Your Creditor

If you’re filing for Chapter 7 or Chapter 13 bankruptcy, the court will appoint a trustee to you. The trustee oversees your case and sells any nonexempt property in order to pay back your creditors.

After your case is filed, the trustee assigned to you will send a letter asking you to send them financial documents. These can include recent bank statements, pay stubs, and tax returns. You must mail the documents promptly according to the specified instructions in the letter.

9. Take Bankruptcy Course 2

Once you file your bankruptcy forms at the courthouse, you need to take another bankruptcy course. This is the Debtor Education Course, which also needs to be completed at an approved agency. Like the first counseling course, you can complete it online or over the phone for between $10 to $50. However, if you are eligible, you can have this fee waived. The course takes at least two hours to complete.

This course does not give you legal advice about the bankruptcy process. Rather, it’s designed to teach you how to make smart financial decisions in the future. You are required to take this course and file your certificate stating you completed it in order to acquire discharge of your medical bills and other debts.

10. Attend the 341 Meeting with Your Trustee

The court will have given you notice about the time, date, and location of your meeting with your trustee, which will take place about a month after you file your case. The primary purpose of the 341 meeting is for the trustee to authenticate your identity and ask you standard questions. Your creditors are allowed to attend and ask you questions about your financial situation, but it is rare for them to appear. Most meetings only take place for about five minutes.

Your U.S. government-issued ID and social security card are essential at this meeting. The 341 meeting cannot go forward if you do not have an approved form of both. You should also bring the documents that the trustee asked for in their letter.

Last Words

For most Americans, filing for medical bankruptcy can feel intimidating, but it can help you find debt relief. With these brief step-by-step instructions, you can potentially file on your own without a costly bankruptcy attorney. However, keep in mind that the above steps are not a replacement for professional legal advice.